A merchant services provider is a company that enables businesses to accept, process, and settle electronic payments through the infrastructure connecting merchants to card networks and issuing banks. Selecting the right provider in 2026 requires evaluating pricing models, security standards, contract terms, and platform integration capabilities simultaneously.

This guide covers provider selection criteria, detailed profiles of eleven leading processors, fee structure comparisons across pricing models, use-case recommendations for omnichannel and high-volume brands, and the operational advantages of unified commerce platforms.

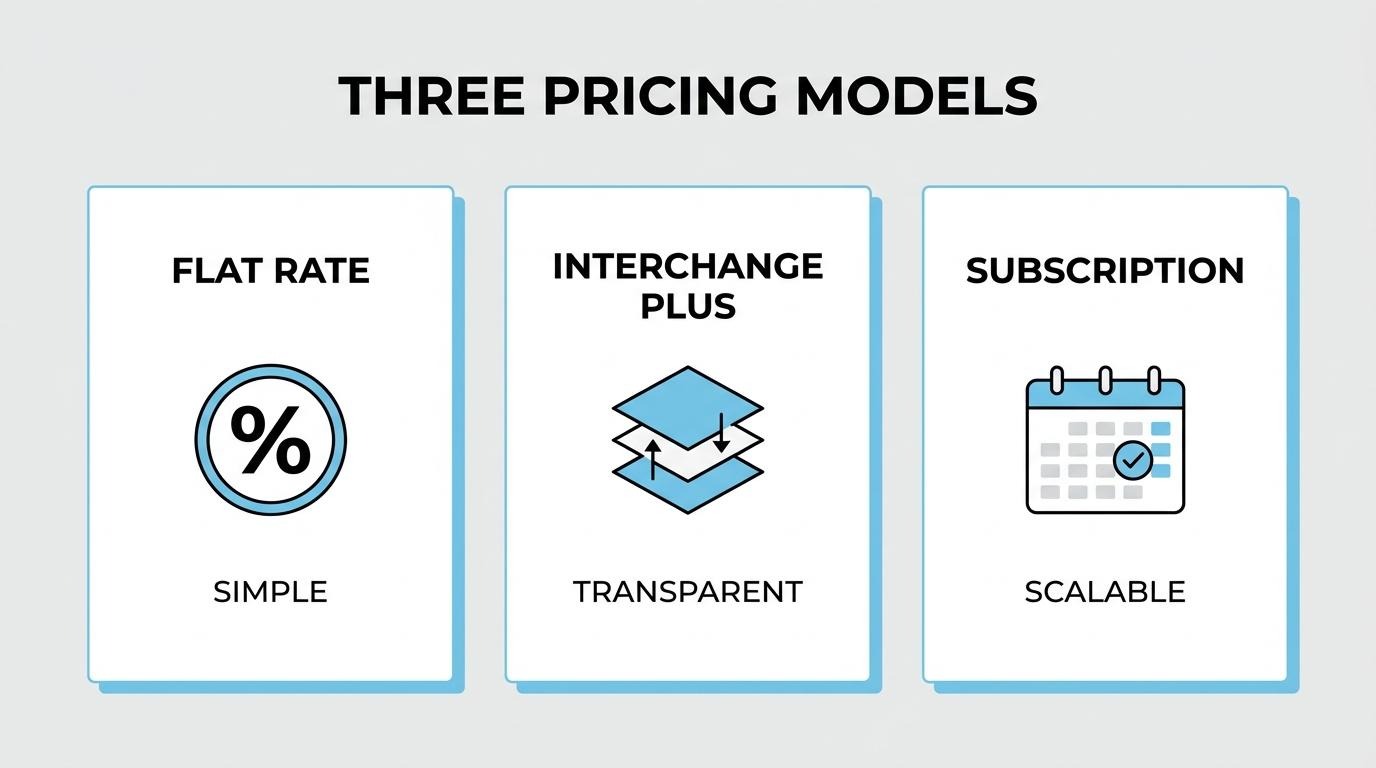

Processing fees vary dramatically by model. Flat-rate providers like Square charge a consistent percentage on every transaction, subscription models like Stax eliminate per-transaction markups in exchange for monthly membership fees, and interchange-plus processors like Helcim and Dharma pass through wholesale card costs with transparent fixed margins. Hidden fees such as PCI non-compliance charges can add nearly 3% to total costs, making pricing transparency a critical differentiator.

Each of the eleven providers profiled serves distinct business stages and channel mixes. SHOPLINE Payments, Square, Stripe, PayPal, Adyen, Helcim, Stax, Chase Payment Solutions, Clover, Payment Depot, and Dharma Merchant Services range from developer-centric API platforms to all-in-one commerce systems with native CRM and subscription billing built into the payment layer.

Contract structures range from month-to-month flexibility with zero termination fees to three-year lock-ins carrying penalties above $400. For scaling brands, this variation determines whether a provider relationship can adapt as transaction volume grows or becomes a costly liability requiring migration.

We also examine how unified commerce architecture, where payments, customer data, and subscription management share one backend, eliminates the reconciliation gaps and tool sprawl that separate integrations create at scale.

A merchant services provider is a company that enables businesses to accept, process, and settle electronic payment transactions, including credit cards, debit cards, and digital wallets. These providers supply the infrastructure connecting merchants to card networks and issuing banks.

According to the Office of the Comptroller of the Currency, merchant processing involves gathering sales information, obtaining authorization, collecting funds from the card-issuing bank, and reimbursing the merchant. This multi-step settlement process happens within seconds at the point of sale, yet involves several distinct intermediaries working behind the scenes.

A merchant services provider typically bundles several core functions:

The distinction between these roles matters. A payment processor manages data flow but is not considered an acquirer unless it operates as a defined financial institution. Some providers, particularly all-in-one platforms, consolidate multiple roles under a single relationship, while others specialize in one layer of the stack.

For scaling ecommerce brands, this distinction shapes everything from fee transparency to data access. Providers that own the full chain often offer tighter integration between commerce operations and payment data, while disaggregated setups require merchants to coordinate between separate vendors.

Understanding what a merchant services provider actually does sets the foundation for evaluating which provider structure best fits a brand's transaction volume, channel mix, and growth trajectory.

Choosing the right merchant services provider matters for ecommerce brands because it directly affects transaction costs, checkout conversion rates, security posture, and operational scalability. The subsections below cover how processing volume amplifies fee differences, why checkout friction drives abandonment, and what hidden costs erode margins.

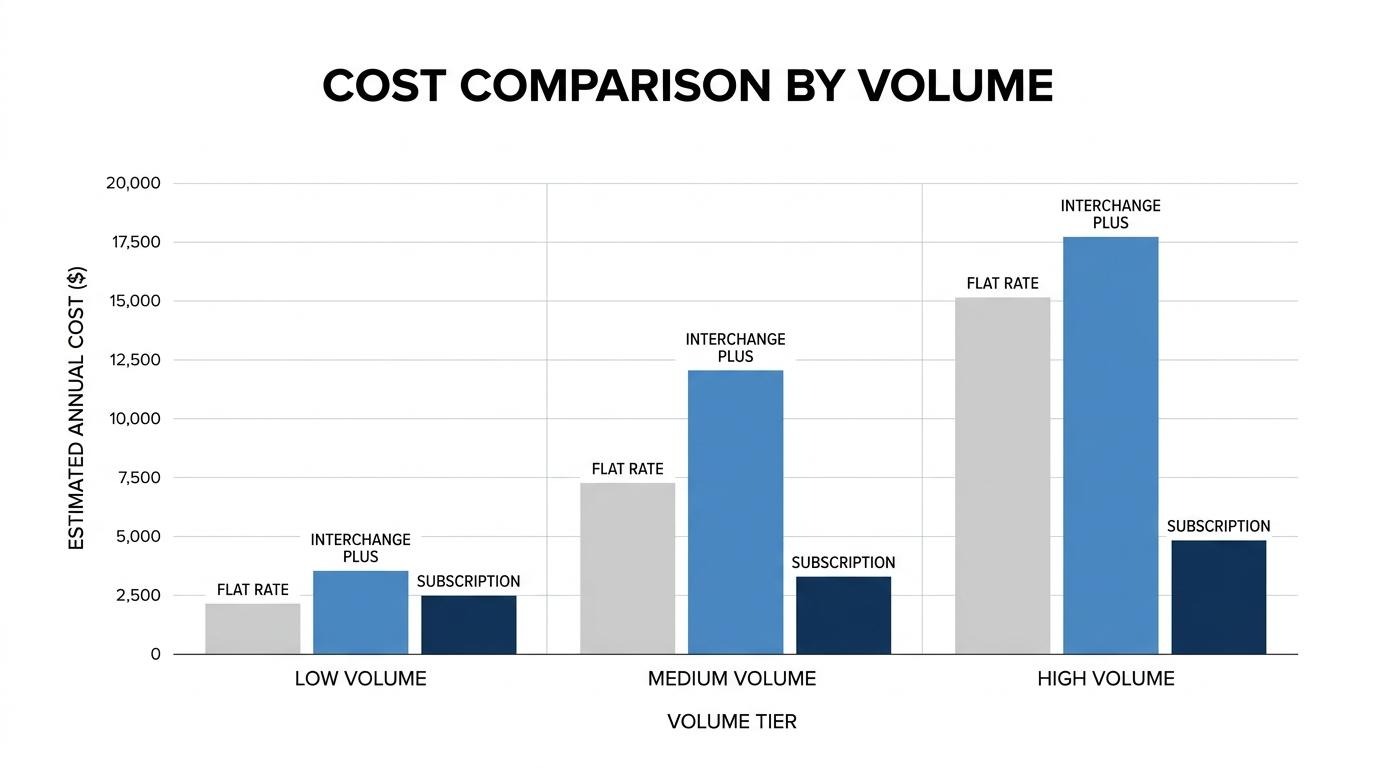

Processing volume amplifies fee differences because even small percentage gaps compound into significant revenue loss at scale. A brand processing $5 million annually loses $50,000 for every additional 1% in effective processing costs. According to Stesanor's 2026 analysis, hidden payment processing fees such as PCI non-compliance and statement fees can add between 0.9% and 2.7% to a merchant's total processing costs. For high-volume DTC brands, selecting the wrong pricing model turns a manageable expense into one of the largest line items on the P&L.

Checkout friction impacts cart abandonment by introducing unnecessary steps, limited payment options, or slow authorization times that cause buyers to leave. The Baymard Institute's meta-analysis of 50 ecommerce studies documents an average online shopping cart abandonment rate of 70.22% by late 2025. While not every abandonment stems from payment issues, a provider that supports fewer payment methods or redirects customers off-site contributes directly to drop-off. Each percentage point recovered at checkout translates into measurable revenue without additional acquisition spend.

Security failures create long-term brand damage because a single data breach erodes customer trust, triggers regulatory penalties, and increases chargeback ratios. Visa reports that tokenized transactions show approximately 30% lower online fraud rates compared to non-tokenized transactions as of early 2026. Providers lacking robust tokenization, PCI DSS v4.0.1 compliance, or real-time fraud detection expose merchants to both financial liability and reputational harm that takes years to reverse.

The right provider supports scale without operational drag by consolidating payment processing, reporting, and channel management into fewer integration points. Global ecommerce sales are forecast to reach $6.88 trillion in 2026, according to Aggentic AI, representing a 7.2% increase from 2025 projections. Brands growing into that expanding market need providers whose infrastructure, contract flexibility, and feature set grow alongside transaction volume rather than creating bottlenecks.

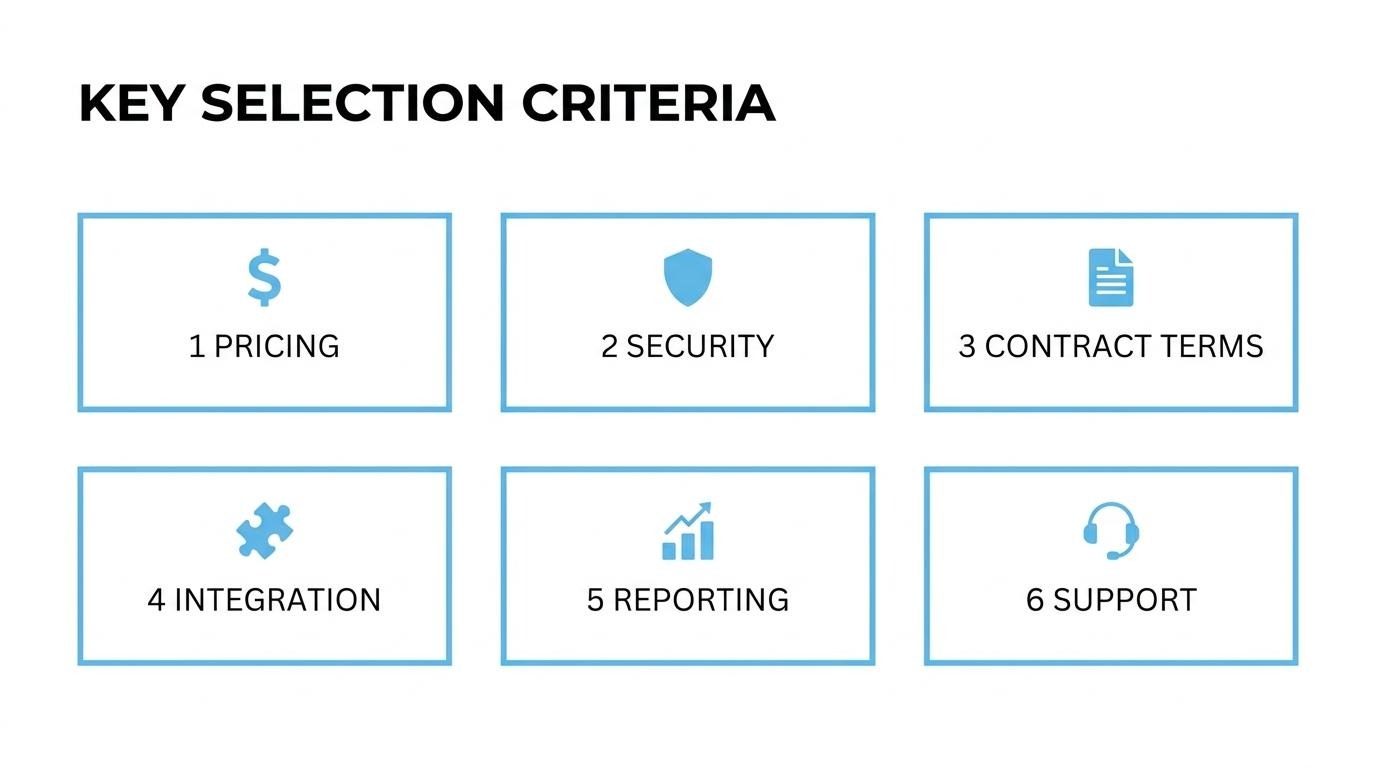

With a clear understanding of why provider choice carries material consequences, the next step is identifying the specific criteria that separate strong options from poor fits.

You should look for transparent pricing, broad payment method support, seamless POS and online integration, strong security compliance, flexible contract terms, and robust reporting. The following subsections break down each criterion.

Processing fees and pricing models compare across three main structures: flat-rate, interchange-plus, and subscription-based. Flat-rate providers like Square bundle software, hardware, and processing into tiered packages, as demonstrated by their 2025 streamlined three-tier framework. Subscription-based models, such as Stax's $99/month plan for businesses processing up to $150,000 annually, charge fixed per-transaction fees of 8 cents (in-person) and 15 cents (keyed-in) on top of wholesale interchange.

Membership models like Payment Depot offer savings for merchants processing $10,000 or more monthly through wholesale interchange rates plus a fixed monthly fee. However, hidden fees remain a significant concern. According to Stesanor, PCI non-compliance charges and statement fees can add 0.9% to 2.7% to total processing costs in 2026. Claims of "0% processing" often mask costs through inflated monthly fees or quiet markups that erode profit margins.

The payment methods and channels supported should include credit cards, debit cards, digital wallets, buy-now-pay-later options, and real-time payment rails. According to yStats, global non-cash transaction volumes are projected to exceed 2.5 trillion transactions by 2028, driven by rapid expansion of digital and real-time payment methods.

Forrester analysts confirm that in the 2026 merchant payment market, supported payment methods, geographic coverage, and settlement options remain the primary drivers for provider choice. A provider that limits accepted methods or lacks coverage in key regions creates friction at checkout and restricts growth potential.

POS and online payment integration is critical for brands selling across physical and digital channels. When payment processing connects directly to both storefront and in-store systems, transaction data flows into a single view without manual reconciliation. Disconnected systems create data silos, inventory mismatches, and fragmented customer records that complicate operations at scale.

Providers offering embedded payment solutions within marketplace or commerce platforms eliminate the need for separate gateway configurations. For brands managing both online and offline sales, native integration reduces development overhead and ensures consistent reporting across channels.

The security and PCI compliance standards required center on PCI DSS v4.0.1, which became mandatory on March 31, 2025. This updated standard introduced requirements for continuous security validation and multi-factor authentication across all system components handling cardholder data, as documented by SecurityMetrics.

Providers should offer tokenization, which replaces primary account numbers with non-sensitive values for recurring billing and refunds. AI-driven fraud detection, end-to-end encryption, and embedded risk management tools are now baseline expectations rather than premium features.

Contract terms and early termination fees differ significantly between providers. Some require multi-year commitments with steep exit penalties, while others operate month-to-month with no cancellation costs.

For scaling brands, long lock-in periods create risk if processing needs change. Prioritizing providers with month-to-month flexibility avoids costly exit scenarios.

You should expect real-time transaction dashboards, customizable reports, exportable data, and granular breakdowns by channel, payment method, and time period. Strong reporting includes chargeback tracking, settlement summaries, and customer-level purchase history.

Providers that consolidate online and in-store transaction data into unified reporting save operational hours otherwise spent reconciling across tools. API access for pulling raw data into business intelligence platforms is essential for high-volume merchants who need custom analytics beyond standard dashboards.

With these selection criteria established, the next step is evaluating specific providers against them.

The best merchant services providers for 2026 span flat-rate, interchange-plus, and subscription pricing models. Each provider below serves different business sizes and selling channels.

SHOPLINE Payments is the native payment processing solution built into the SHOPLINE ecommerce platform. It eliminates the need for third-party gateway integrations by handling transactions within the same system that manages storefront, CRM, and marketing. The Advanced plan offers local online processing at 2.4% + USD 0.25 and local POS or retail processing at 2.4% + USD 0.10 per transaction, with support for major credit cards and digital wallets. Because payments, customer data, and order management share one backend, merchants avoid the reconciliation gaps that emerge when stitching separate tools together. For scaling DTC brands already operating on SHOPLINE, this removes one more external dependency from the stack.

Square is a flat-rate payment processor that bundles hardware, software, and processing into unified tiers. In-person transactions cost 2.6% + $0.10, online payments run 2.9% + $0.30, and keyed-in transactions are 3.5% + $0.15. Square requires no monthly fees on its base plan, making it accessible for businesses with lower transaction volumes. The platform includes a free POS system, invoicing tools, and an online store builder. Square works best for small to mid-sized retailers and service businesses that value simplicity over granular rate negotiation.

Stripe is a developer-centric payment infrastructure provider that powers online and in-app transactions globally. Businesses running on Stripe generated $1.9 trillion in total volume in 2025, representing a 34% increase from 2024, according to FXC Intelligence. Standard processing is 2.9% + $0.30 for online card payments. Stripe's strength lies in its extensive API library, which supports custom checkout flows, marketplace payouts, and multi-currency settlement. The platform also handles subscription billing natively, with tools for revenue recovery and usage-based pricing. Stripe suits brands with development resources that need deep customization.

PayPal Commerce Platform is a unified payments ecosystem that combines checkout, Venmo, buy-now-pay-later, and merchant tools under one integration. Standard domestic transaction fees are 2.99% for goods and services, while Venmo transactions for merchants cost 3.49% plus a fixed fee. PayPal is building a next-generation commerce platform that includes multi-year partnerships and expanding Venmo's peer-to-peer network into commerce, according to its Q1 2026 earnings presentation. The platform's buyer network of over 400 million active accounts gives merchants built-in demand. For brands prioritizing checkout conversion through familiar payment options, PayPal reduces friction at the point of sale.

Adyen is an enterprise-grade payment platform that operates on an Interchange++ pricing model, where the acquirer fee starts at 0.60% per transaction based on monthly card volume. Unlike many competitors, Adyen contracts carry no early termination fees, with either party able to terminate upon notice. The platform processes payments across 30+ countries through a single integration, supporting local acquiring in each market. Adyen's embedded risk management tools use machine learning to detect fraud in real time. This provider targets high-volume merchants and global brands that need localized payment methods without managing multiple regional processors.

Helcim is an interchange-plus processor with no monthly fees, no contracts, and no cancellation penalties. Its Smart Terminal hardware costs $349 per unit or $32 per month on a one-year plan. Processing rates decrease automatically as monthly volume increases, making Helcim progressively cheaper for growing businesses. The platform includes built-in POS software, online invoicing, and a hosted payment page. Helcim fits small to mid-sized businesses, particularly retail and simple food-service operations, that want transparent pricing without negotiating custom rates.

Stax operates a subscription-based pricing model that charges 0% markup on interchange rates in exchange for a flat monthly fee. Plans start at $99 per month for businesses processing up to $150,000 annually, with per-transaction fees of $0.08 for in-person and $0.15 for keyed-in cards. The platform includes invoicing, payment links, and reporting software within the subscription. Stax works best for established businesses with consistent monthly volume, where the fixed subscription cost is offset by savings on per-transaction markups.

Chase Payment Solutions is a bank-backed processor that leverages Chase's existing merchant banking relationships. The platform typically requires a 3-year contract and may charge an early termination fee of $295 to $495 if cancelled before term, according to Merchant Insiders. QuickAccept hardware includes a card reader at $99 and a base at $49, or $129 bundled. Chase suits businesses already banking with JPMorgan Chase who value same-day deposit access and consolidated financial management. The trade-off is less pricing flexibility compared to independent processors.

Clover is a POS-first payment platform offering proprietary hardware and integrated processing. Hardware costs in 2026 include approximately $1,800 for the Station Solo, $800 for the Mini Gen 3, and $600 for the Flex Gen 4. Clover supports a marketplace of third-party apps for inventory, loyalty, and employee management. Processing rates vary by plan and reseller, which can make true cost comparisons difficult. Clover targets brick-and-mortar businesses, restaurants, and service providers that need robust in-store hardware with software extensibility.

Payment Depot is a membership-based processor owned by Stax that passes wholesale interchange rates directly to merchants. According to Best CCP, Payment Depot's 2026 basic plan costs $49 per month with a per-transaction fee of interchange plus $0.15. Businesses processing $10,000 or more monthly typically realize savings compared to flat-rate models. The platform supports virtual terminals, mobile processing, and integrations with popular shopping carts. Payment Depot suits mid-volume merchants who want interchange-plus transparency without negotiating enterprise contracts.

Dharma Merchant Services is a registered B-Corp offering interchange-plus pricing with a focus on ethical business practices. Ecommerce merchants pay 0.20% + $0.11 per authorization with a fixed monthly fee of $20, according to Dharma's published rate schedule. Dharma maintains a 4-star rating on Trustpilot based on 140 verified merchant reviews. The provider supports retail, restaurant, and online businesses with month-to-month contracts and no early termination fees. For brands that value corporate responsibility alongside competitive rates, Dharma offers a distinctive positioning in the merchant services landscape.

With each provider's core model outlined, direct fee comparisons reveal where savings compound at different volume tiers.

These merchant services providers compare on fees across three pricing models: flat-rate, interchange-plus, and subscription-based. Each structure suits different transaction volumes and business stages.

Flat-rate pricing providers' typical costs are a fixed percentage plus a per-transaction fee on every sale, regardless of card type. Square charges 2.6% + $0.10 for in-person transactions and 2.9% + $0.30 online. PayPal's standard domestic rate sits at 2.99% for goods and services, while Venmo transactions cost 3.49% plus a fixed fee. SHOPLINE's Advanced plan applies 2.4% + $0.30. These models offer predictability but become expensive as volume grows, since merchants pay the same rate whether the underlying interchange is 0.5% or 2.1%.

Interchange-plus providers' typical costs are the actual interchange fee set by card networks plus a fixed markup from the processor. Adyen starts its acquirer markup at 0.60% per transaction, scaled by monthly card volume. Dharma Merchant Services charges interchange plus 0.20% + $0.11 per authorization for ecommerce merchants, with a $20 monthly fee. Helcim uses interchange-plus with no monthly fee. For high-volume DTC brands processing above $50,000 monthly, this model often delivers the lowest effective rate because the markup stays constant while interchange varies by card type.

Subscription-model providers' typical costs are a flat monthly membership fee plus interchange at wholesale rates and a small per-transaction surcharge. According to NerdWallet, Stax's pricing starts at $99 per month for businesses processing up to $150,000 annually, with per-transaction fees of $0.08 in-person and $0.15 keyed-in. Payment Depot offers a $49 monthly plan at interchange plus $0.15 per transaction. Because the monthly fee replaces percentage-based markups, merchants processing higher volumes retain more margin on each sale.

Understanding which fee structure aligns with your sales volume helps narrow the provider field before evaluating features.

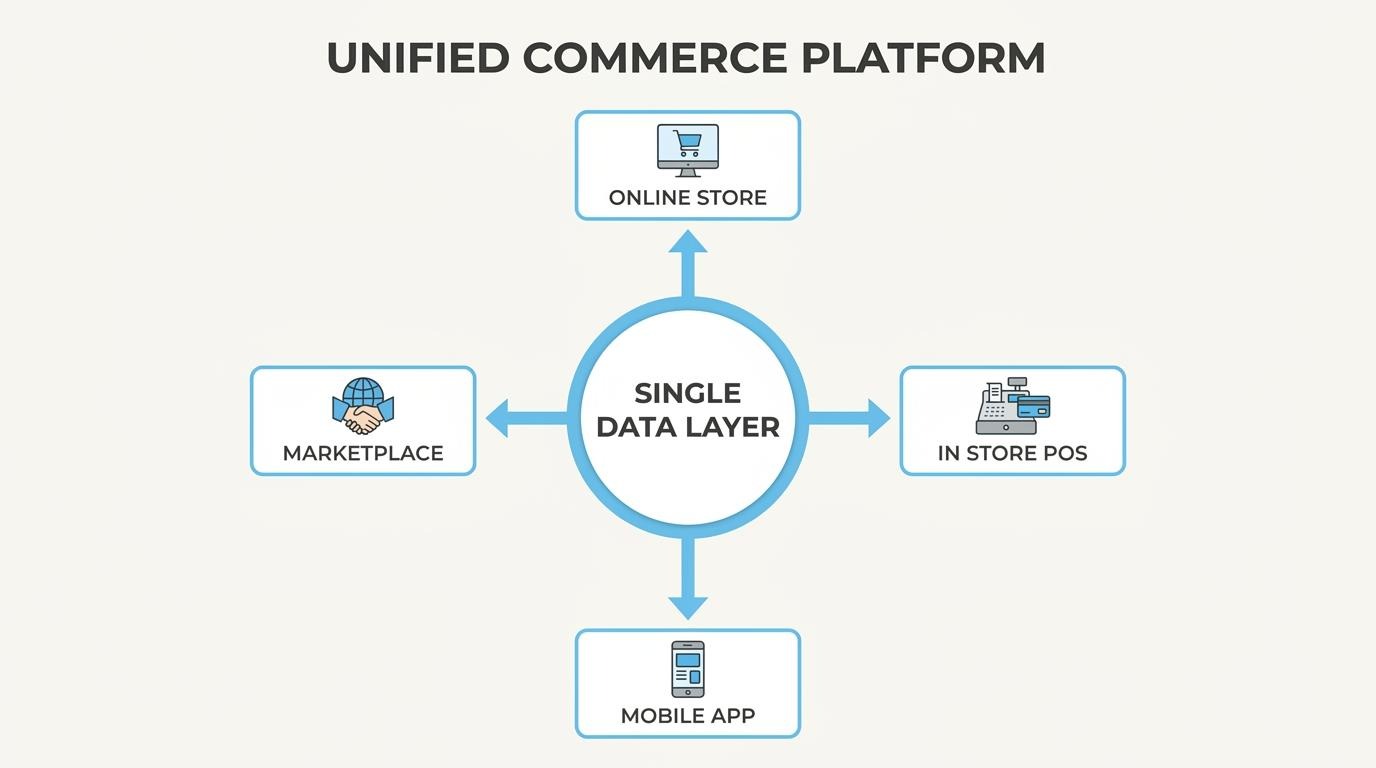

The best merchant services provider for omnichannel selling is one that unifies online, in-store, and mobile transactions under a single data layer. Providers with native POS integration, shared inventory, and consolidated customer records eliminate the friction of managing separate systems across channels.

According to a 2025 industry benchmark study of 220 North American retailers, only 17% currently rate their unified commerce capabilities as mature, despite clear revenue benefits. Retailers utilizing unified commerce systems report up to 30% higher customer lifetime value compared to those with siloed systems. This gap signals that most merchants still operate fragmented stacks where online and offline data never resolve to the same customer profile.

Adyen, Square, and SHOPLINE each approach omnichannel differently:

For brands processing meaningful volume across both digital and physical channels, the deciding factor is not just payment acceptance. It is whether customer data, inventory, and marketing automation stay unified without requiring middleware or third-party syncs. That operational simplicity becomes increasingly valuable as order volume and channel count grow together.

The best merchant services provider for high-volume DTC brands is one offering interchange-plus pricing, volume-based rate negotiation, and unified commerce infrastructure. Providers like Adyen and Stax serve this segment most directly, though the right choice depends on monthly volume thresholds and channel complexity.

High-volume DTC brands processing above $500,000 monthly lose significant margin on flat-rate models. Interchange-plus structures pass through wholesale card costs with a transparent markup, making per-transaction savings compound at scale. According to Business.com, competitive reviews on sites like Forbes Advisor and NerdWallet often emphasize SMB-friendly flat-rate models but lack detailed analysis of enterprise-grade interchange-plus structures for high-volume DTC brands.

For brands at this revenue tier, the provider decision hinges on three factors:

Flat-rate simplicity benefits smaller merchants, but high-volume operators need granular cost control and consolidated reporting across channels. The gap between a 2.9% flat rate and a negotiated interchange-plus structure of 1.8% + $0.10 represents tens of thousands in annual savings at scale. Brands processing at this level should treat payment processing as a margin lever, not a commodity checkbox.

With processing costs optimized, recurring billing capabilities become the next critical differentiator for subscription-driven DTC brands.

Merchant services providers handle recurring and subscription billing through automated payment scheduling, tokenized card storage, and dunning management tools that retry failed charges without manual intervention.

Recurring billing requires securely storing customer payment credentials for repeated charges on a fixed schedule. Tokenization replaces primary account numbers (PAN) with alternative values that can be used for voids, refunds, and recurring billing without storing sensitive card data. This approach satisfies PCI compliance requirements while enabling seamless monthly or weekly charge cycles.

Failed payments represent one of the largest sources of involuntary churn for subscription businesses. According to Flexprice, Stripe's machine-learning dunning engine, Smart Retries, recovers an average of 56% of failed recurring payments for subscription-based businesses. Providers vary widely in dunning sophistication; some offer basic fixed-interval retries, while others use behavioral signals to optimize retry timing.

Key capabilities to evaluate in a subscription billing provider include:

For brands running subscriptions at scale, the difference between a basic retry system and an intelligent dunning engine can translate directly into retained revenue. Platforms with native subscription infrastructure tend to reduce the integration complexity that comes from bolting third-party tools onto a separate payment processor.

Understanding how providers manage recurring billing helps clarify which mistakes to avoid when evaluating the full merchant services relationship.

Common merchant services provider mistakes to avoid include ignoring hidden fees, overlooking contract lock-ins, choosing based on advertised rates alone, neglecting PCI compliance, and failing to plan for scalability. Each of these errors can quietly erode margins or create operational friction that compounds over time.

The most costly mistakes fall into these categories:

For brands processing at scale, one of the most underestimated mistakes is selecting a payment provider in isolation from the broader commerce stack. When payments, CRM, and order data live in separate systems, reconciliation gaps and data silos emerge quietly and become expensive to fix later.

Understanding these pitfalls sets the stage for a smooth transition when switching providers becomes necessary.

You switch merchant services providers without disrupting sales by running parallel processing, migrating token data carefully, and timing the cutover during a low-traffic window. The steps below cover each phase of a clean transition.

Merchant processing involves settling credit and debit card transactions through card associations: gathering sales information, obtaining authorization, collecting funds from the issuing bank, and reimbursing the merchant. Because this chain depends on multiple parties, a poorly timed switch can interrupt any link in that sequence and stall revenue.

A structured migration follows these steps:

Token migration is the most time-sensitive phase. According to a Razorpay payment processing migration checklist, this step typically takes several weeks to ensure data integrity and prevent service downtime. Rushing it risks failed recurring charges and involuntary churn among subscription customers.

For brands operating at scale with thousands of stored cards and active subscriptions, the parallel-processing window is not optional; it is the difference between a seamless switch and a revenue gap that compounds daily. Planning the cutover for a historically low-sales day, such as midweek outside of promotional periods, further reduces exposure.

With a clean switch complete, the next consideration is whether your new payment processing should live inside your commerce platform rather than alongside it as a separate tool.

Payment processing inside your commerce platform eliminates the middleware, data silos, and sync failures that separate tool stacks create. Below, we cover how SHOPLINE consolidates payments, CRM, and subscriptions natively, followed by key takeaways from the full provider landscape.

SHOPLINE handles payments, CRM, and subscriptions within a single system architecture where all three functions share one customer data layer. A payment gateway is a system of technologies and processes that allows merchants to electronically submit transactions to processing networks such as the Credit Card Interchange and ACH Network; on SHOPLINE, this gateway connects directly to native CRM records and subscription logic without third-party connectors.

This means every transaction updates customer profiles, triggers lifecycle automation, and manages recurring billing from one backend. Brands processing real volume no longer reconcile data across separate payment apps, email platforms, and subscription tools. For operators scaling past $1M in annual revenue, that consolidation removes the brittleness and cost of maintaining five to fifteen disconnected integrations.

The key takeaways about the best merchant services providers for 2026 are:

According to J.D. Power's 2026 U.S. Merchant Services Satisfaction Study, large U.S. banks currently lead specialized payment processors in overall merchant satisfaction scores. For high-growth DTC brands, however, satisfaction often hinges less on traditional banking relationships and more on whether the provider eliminates tool sprawl while maintaining competitive processing economics.