Ecommerce accounting is the practice of tracking, categorizing, and reporting all financial transactions generated by an online store, including digital sales revenue, payment gateway fees, refunds, inventory costs, and platform-specific charges across multiple channels.

This guide covers accounting methods and IRS thresholds, core financial statements, sales tax and multi-state compliance, payment processing and inventory accounting, revenue recognition standards, common bookkeeping mistakes, supporting tools, and unified commerce workflows.

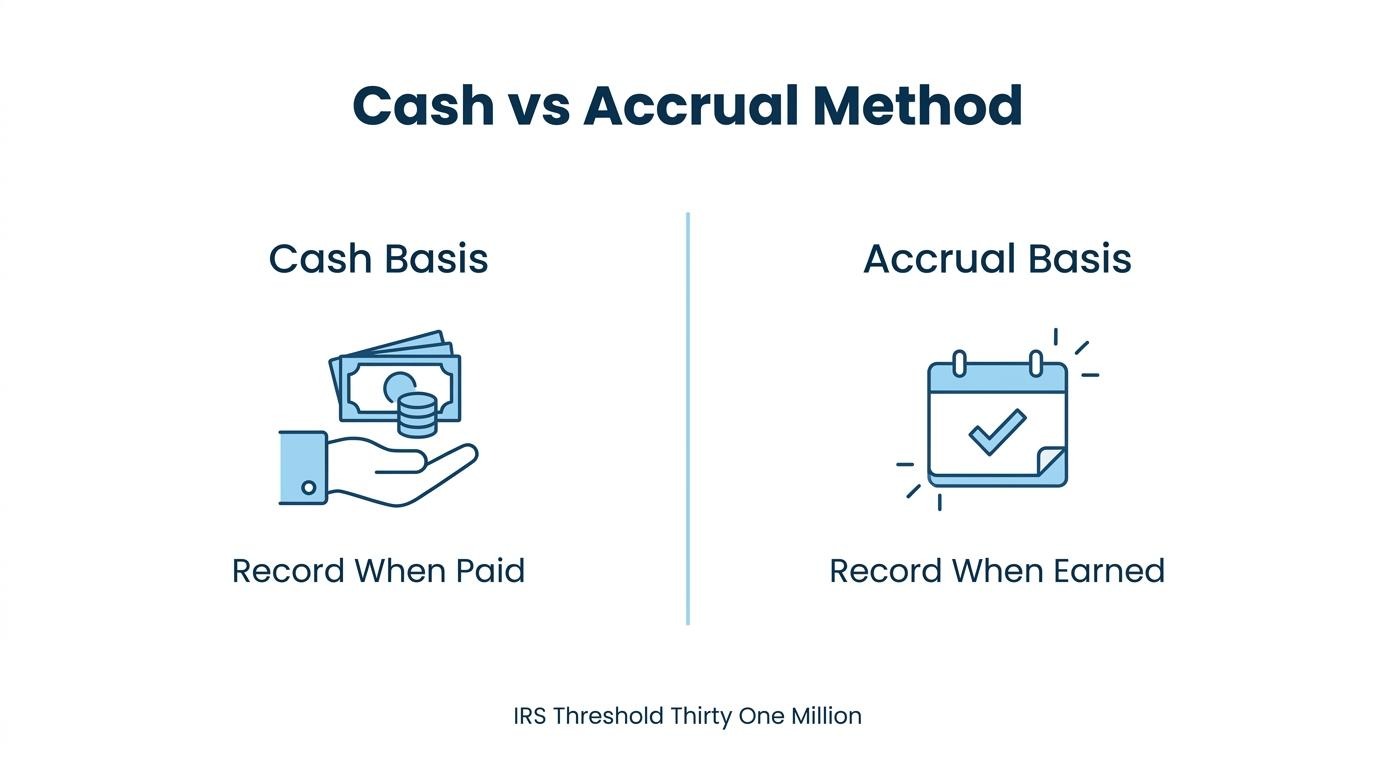

Cash basis accounting records revenue when payment arrives, while accrual basis matches revenue to the period it was earned. The IRS mandates accrual for businesses exceeding $31 million in gross receipts, but growing DTC brands often switch earlier because inventory timing gaps distort cash-basis reporting.

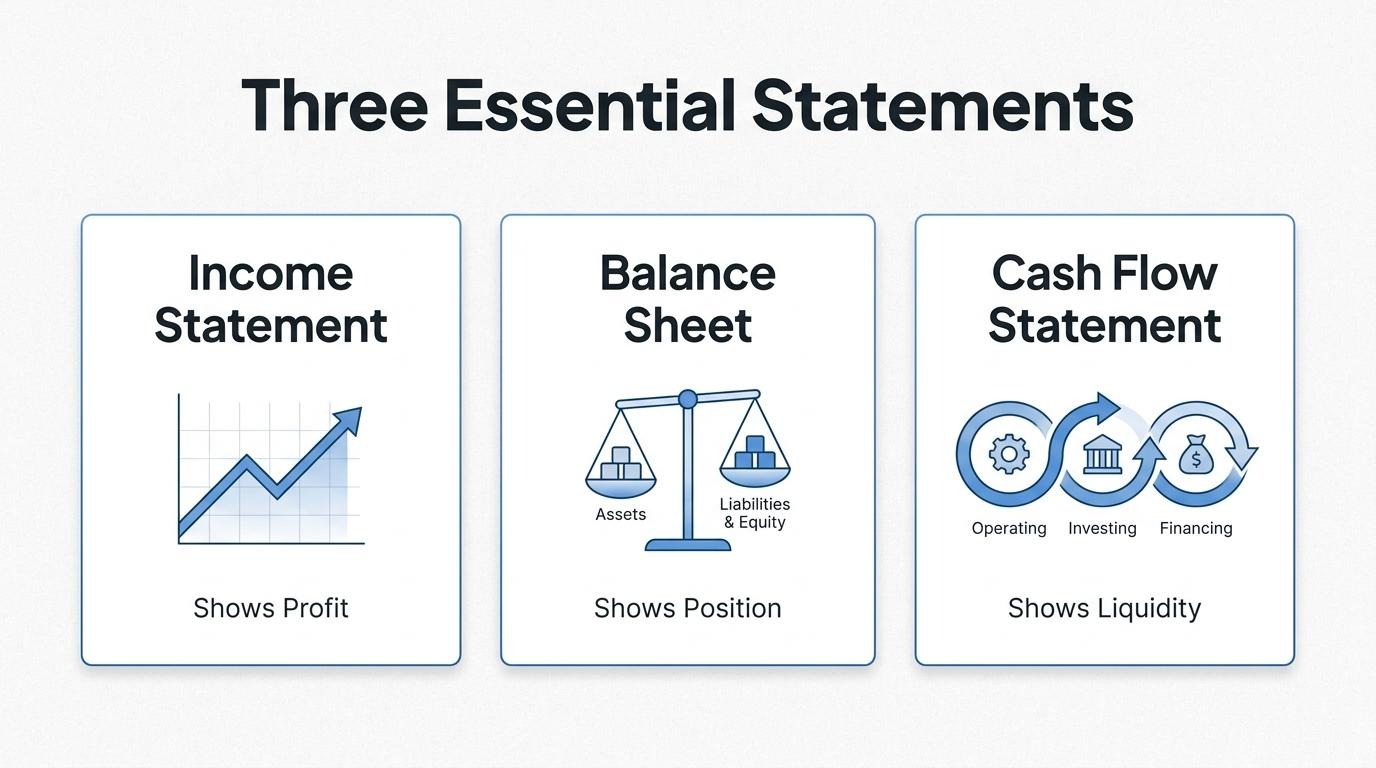

Three financial statements form the foundation of ecommerce reporting: the income statement, balance sheet, and cash flow statement. Together they reveal profitability, financial position, and liquidity across every sales channel.

Sales tax compliance requires understanding economic nexus thresholds, which most states set at $100,000 in sales or 200 transactions. Sellers must register, collect, and remit tax in every state where they trigger nexus, making automation essential once obligations span more than a few jurisdictions.

Payment processing fees, COGS calculations, and inventory shrinkage each demand precise categorization to prevent distorted margins. Revenue recognition under ASC 606 adds further complexity for subscriptions, gift cards, and pre-orders, where payment precedes fulfillment.

Common mistakes like commingling funds, skipping reconciliation, and miscategorizing expenses compound quickly at scale. Consolidating orders, subscriptions, and POS data into a unified commerce system eliminates manual reconciliation and reduces the compliance risk that fragmented tools create.

Ecommerce accounting involves tracking digital sales revenue, payment gateway fees, refunds, inventory costs, and platform-specific charges across multiple channels. The following sections break down how it differs from traditional accounting, what transactions require tracking, and why DTC brands face added complexity.

Ecommerce accounting differs from traditional accounting by managing digital transactions, including payment gateway processing, fee deductions, and delayed lump-sum payouts, rather than straightforward physical-store transactions. According to E2E Accounting, ecommerce accounting is characterized by increased transaction volumes, diverse payment gateways, specific online sales taxes, and various platform fees that have no equivalent in brick-and-mortar bookkeeping.

Key distinctions include:

This complexity also makes hiring harder; specialist ecommerce accounting positions require an average of 73 days to fill due to a CPA shortage in the U.S.

The financial transactions ecommerce sellers must track include sales revenue, refunds, inventory costs, and platform-specific fees. According to VBS Global, ecommerce sellers are required to meticulously track these categories, including fees associated with services like Amazon FBA.

Essential transaction categories include:

Missing even one category distorts profitability reporting, making it impossible to identify which products or channels actually generate margin.

Ecommerce accounting is more complex for DTC brands because these businesses own the entire customer lifecycle, from acquisition through fulfillment and post-purchase retention, creating financial touchpoints that wholesale or marketplace-only sellers never encounter.

DTC-specific complexity drivers include:

For brands scaling past $1M in revenue, these overlapping obligations compound quickly. Consolidating commerce, order management, and customer data into fewer systems reduces the reconciliation burden that fragments financial clarity across disconnected tools.

An ecommerce business should use either cash basis or accrual basis accounting, depending on revenue size and operational complexity. The IRS sets specific thresholds that determine eligibility.

Cash basis accounting works for ecommerce by recording revenue when IRSpayment is received and expenses when they are paid. An online store records a sale only when the payment processor deposits funds, not when the order ships. This method simplifies bookkeeping because it tracks actual cash movement rather than obligations.

According to Block Advisors, the IRS permits businesses with average annual gross receipts of $31 million or less over the preceding three tax years to utilize the cash method for 2025. Most early-stage ecommerce sellers qualify under this threshold, making cash basis the simpler starting point for stores with straightforward transaction patterns and minimal inventory complexity.

Accrual basis accounting works for ecommerce by recording revenue when earned and expenses when incurred, regardless of when cash changes hands. A DTC brand records a sale at order confirmation, even if the payment gateway holds funds for several days before settlement.

Businesses whose gross receipts exceed $31 million in 2025 are mandated by the IRS to employ the accrual method. Even below that threshold, accrual accounting gives a more accurate picture of profitability because it matches revenue against the costs that generated it within the same period. For inventory-heavy sellers, this alignment prevents misleading profit snapshots that cash basis can produce during high-growth months.

Growing DTC brands typically need accrual basis accounting. Once a brand carries significant inventory, manages subscriptions, or processes high order volumes, cash basis distorts the true financial picture by misaligning revenue timing with associated costs.

Accrual accounting matches each sale to its fulfillment cost, platform fees, and returns within the same reporting period. This accuracy becomes essential when:

For brands scaling past the early stage, switching proactively to accrual avoids a disruptive mid-growth conversion later. Understanding your accounting method also determines how you structure financial statements.

The core financial statements every ecommerce seller needs are the income statement, the balance sheet, and the cash flow statement. These three reports together reveal profitability, financial position, and liquidity.

The income statement, also known as the profit and loss statement, measures revenue minus expenses over a specific period. For ecommerce sellers, this report captures gross sales, returns, cost of goods sold, platform fees, shipping costs, and marketing spend. The result is net profit or net loss. Reviewing the income statement monthly helps sellers identify which product lines generate margin and which erode it. Without this visibility, scaling decisions rely on guesswork rather than actual performance data.

The balance sheet shows what a business owns, what it owes, and the owner's equity at a single point in time. Assets include inventory, cash, and accounts receivable from marketplace payouts not yet deposited. Liabilities cover outstanding supplier invoices, sales tax collected but not yet remitted, and any business loans. For DTC brands carrying significant inventory, this statement reveals whether growth is funded sustainably or stretching the business thin.

The cash flow statement tracks actual money entering and leaving the business across operating, investing, and financing activities. According to BPlanWriter, 82% of business failures are attributed to inadequate cash flow management. This makes the cash flow statement arguably the most critical report for ecommerce sellers, where timing gaps between paying suppliers and receiving marketplace payouts create liquidity risk. A 2025 survey by BILL found that 6 out of 10 financial leaders prioritize cash flow management as their primary concern. Monitoring this statement weekly, not just monthly, gives sellers early warning before shortfalls become crises.

With financial statements providing the full picture, understanding sales tax obligations protects that clarity from compliance surprises.

You should handle sales tax in ecommerce accounting by understanding nexus rules, tracking multi-state obligations, and automating collection where possible. The following sections cover economic nexus thresholds, multi-state compliance, and when automation becomes necessary.

Economic nexus is a tax obligation triggered when a business exceeds specific sales thresholds in a state, even without physical presence there. Most states set these thresholds at $100,000 in sales and/or 200 transactions within a given year, according to Avalara's state-by-state guide. Once crossed, the seller must register, collect, and remit sales tax in that state.

Thresholds are not static. Effective January 1, 2025, Alaska eliminated its 200 transactions threshold entirely, requiring only a revenue-based trigger. Other states periodically adjust their rules, making ongoing monitoring essential for any ecommerce brand selling across state lines.

Multi-state sales tax obligations work by requiring ecommerce sellers to collect and remit tax in every state where they have established economic nexus. Each state sets its own rates, product taxability rules, and filing frequencies.

Key compliance requirements include:

For brands selling in 10, 20, or more states simultaneously, manual tracking becomes impractical quickly. This complexity is one reason growing DTC operations often consolidate their commerce and order data into a single system rather than reconciling sales figures across disconnected tools.

You should automate sales tax collection once you have nexus in more than two or three states. At that point, manually applying correct rates, tracking threshold changes, and filing returns on time becomes error-prone and operationally expensive.

Automation tools like Avalara, TaxJar, or native platform integrations handle rate calculation, exemption certificates, and return filing. They sync with your ecommerce platform to apply real-time rates at checkout based on the buyer's location. For most scaling brands, the cost of automation is far lower than the penalty risk of late or incorrect filings; non-compliant ecommerce operations can face fines up to $25,000.

With tax collection automated, accurate bookkeeping for payment processing fees becomes the next accounting priority.

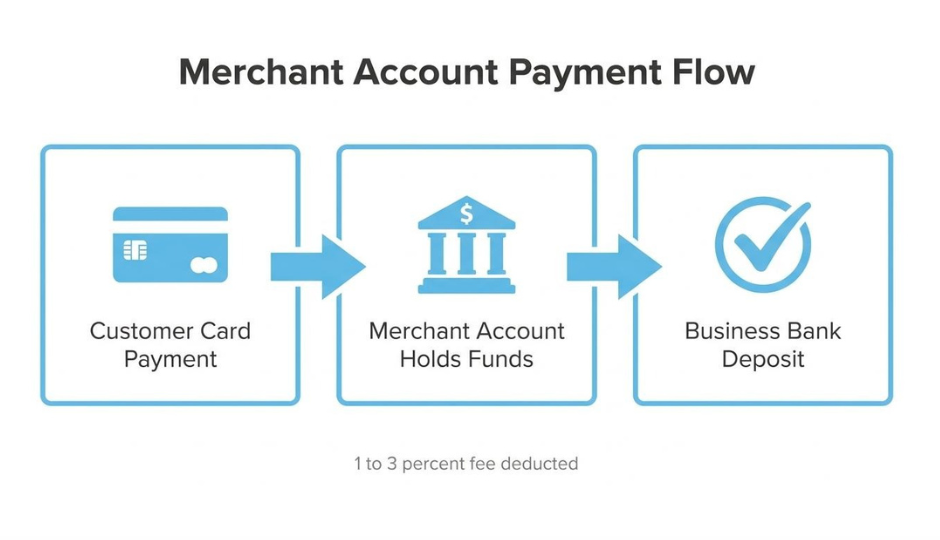

Payment processing and platform fees are recorded as business expenses that reduce net revenue on your income statement. The sub-sections below cover how to record gateway fees and how chargebacks and refunds affect your books.

Gateway and transaction fees should be recorded as a separate expense line item, typically labeled "Payment Processing Fees" or "Merchant Fees," in your chart of accounts. Each time a payment processor deducts its percentage, you record gross revenue as income and the fee as an operating expense.

Common fee structures include:

Never record the net deposit as your total revenue. Separating gross sales from processing fees gives you accurate margin visibility and simplifies tax preparation.

Chargebacks and refunds affect your books by reversing previously recognized revenue and introducing additional fee expenses. When a customer initiates a refund, you reduce sales revenue and restore inventory value on the balance sheet. When a chargeback occurs, the reversal includes the original transaction amount plus a dispute fee from your processor.

Key accounting impacts include:

Tracking these separately from general expenses prevents distorted profitability reporting. For brands processing high volumes across multiple channels, consolidating this data into one system eliminates reconciliation gaps that compound at scale.

Ecommerce businesses should manage inventory accounting by calculating COGS accurately, selecting a consistent costing method, and recording shrinkage promptly. The following subsections cover COGS calculation, FIFO versus weighted average costing, and shrinkage write-offs.

Cost of goods sold (COGS) is the direct cost attributable to products sold during a specific period. COGS includes raw materials, manufacturing labor, and inbound shipping tied to inventory.

The standard formula is:

Accurate COGS calculation requires consistent inventory counts and proper categorization of direct costs. Indirect expenses like marketing or warehousing rent do not belong in COGS; they fall under operating expenses on the income statement. For DTC brands selling physical products, miscalculating COGS distorts gross margin and leads to misinformed pricing decisions.

FIFO (First-In, First-Out) assumes the oldest inventory units sell first, while weighted average cost (WAC) assigns a blended per-unit cost across all available stock. Each method affects reported gross profit differently when purchase prices fluctuate.

Most ecommerce sellers find WAC operationally simpler, though FIFO provides more precise margin visibility when supplier pricing shifts frequently.

Inventory shrinkage is accounted for by adjusting inventory records downward and recording the loss as an expense. Shrinkage encompasses theft, damage, administrative errors, and spoilage that reduce actual stock below recorded levels.

According to Opensend, acceptable industry benchmarks for inventory shrinkage typically range from 0.5% to 2% of total inventory value. Exceeding this range signals process failures that require investigation.

To record shrinkage:

Write-offs for obsolete or unsaleable stock follow the same journal entry structure but may require a separate reserve account when losses are predictable. Regular cycle counts, rather than annual counts alone, catch discrepancies before they compound into material misstatements.

With inventory valuation methods established, revenue recognition rules determine when those sales actually hit the books.

Revenue recognition challenges in ecommerce arise from transactions where payment occurs before the performance obligation is fulfilled. ASC 606 governs how and when sellers record revenue from subscriptions, gift cards, and pre-orders.

Revenue from subscriptions is recognized ratably over the service period, not at the point of initial payment. ASC 606 requires sellers to identify each performance obligation within the subscription contract and allocate revenue as those obligations are satisfied. A monthly subscription box, for example, generates recognizable revenue only when each box ships. Annual plans paid upfront create a contract liability on the balance sheet, with revenue released monthly as fulfillment occurs. This distinction matters because recording the full payment as immediate revenue overstates income and distorts monthly profitability.

Gift cards and store credit should be recorded as contract liabilities at the time of sale, not as revenue. According to Houseblend's analysis of ASC 606 compliance, a gift card sale represents a prepayment for a future performance obligation, meaning revenue recognition occurs only when the card is redeemed. Store credits issued for returns follow the same principle. Unredeemed balances remain as liabilities until breakage (the estimated portion that will never be redeemed) is recognized over time based on historical redemption patterns.

Revenue for pre-orders and backorders is recognized when control of the product transfers to the customer, typically at shipment or delivery. Collecting payment at order placement creates a contract liability identical in treatment to gift cards. The key distinction is that pre-orders have an identifiable future fulfillment date, while backorders depend on inventory availability. Neither scenario permits revenue recognition at checkout because the seller has not yet satisfied the performance obligation. For DTC brands running frequent product launches, properly deferring pre-order revenue prevents significant period-over-period reporting distortions.

With revenue timing clarified, avoiding common accounting mistakes protects the accuracy these standards require.

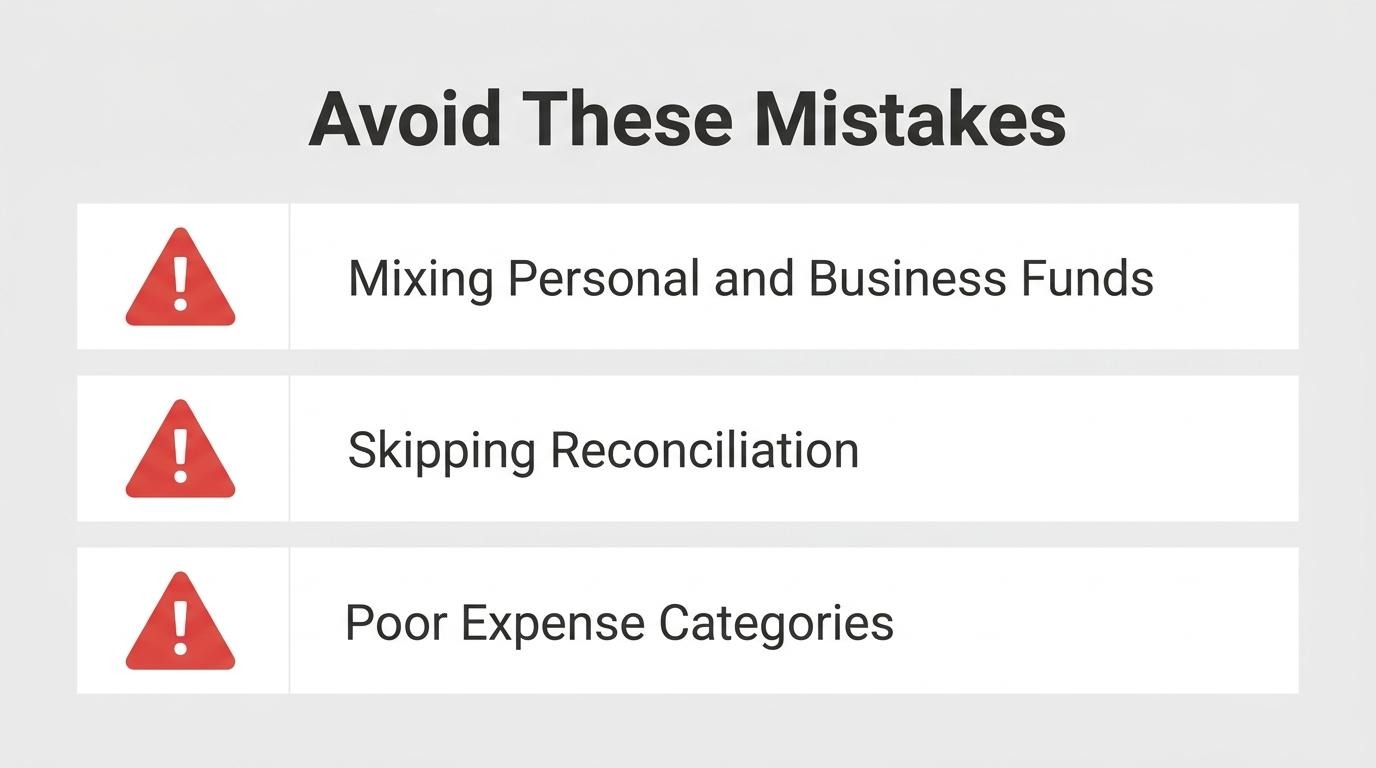

The most common ecommerce accounting mistakes involve commingling funds, skipping reconciliation, and miscategorizing transactions. Each error compounds over time, distorting financial clarity.

Mixing personal and business finances is risky because it destroys audit trails, complicates tax filings, and can pierce the liability protection of your business entity. When personal purchases flow through a business account, every transaction requires manual review to separate deductible expenses from personal spending.

According to BPlanWriter, 82% of business failures are attributed to inadequate cash flow management. Commingled accounts make cash flow nearly impossible to measure accurately, since personal withdrawals mask true operating burn. A dedicated business bank account and credit card are the minimum foundation for reliable ecommerce bookkeeping.

Ignoring reconciliation cycles allows discrepancies between your accounting records and actual bank or platform payouts to accumulate undetected. Payment processors like Stripe and PayPal batch transactions, deduct fees, and hold reserves before depositing funds. Without regular reconciliation, missing refunds, duplicate entries, and unrecorded chargebacks quietly erode accuracy.

For context, platforms often net fees directly from payouts; Shopify Payments, for instance, charges starting at 2.7% + $0.30 per online transaction. Those deductions never appear as separate line items unless you reconcile payout reports against your ledger. Weekly or biweekly reconciliation catches errors before month-end close becomes an archeological dig.

Poor categorization distorts profitability by misallocating expenses across accounts, which inflates some margins while hiding true costs in others. Labeling shipping supplies as "office expenses" or grouping platform fees with advertising spend makes your income statement unreliable for decision-making.

Common categorization errors include:

When categories lack precision, gross margin and net profit percentages become meaningless. Standardized chart-of-accounts templates designed for ecommerce resolve most of these issues before they compound.

With common mistakes identified, the right tools and workflows help prevent them systematically.

Ecommerce accounting tools include dedicated software like QuickBooks and Xero, middleware connectors such as A2X, and platform-native reporting features. The sections below cover how integrations sync data and when hiring a specialist makes sense.

Accounting integrations work by automatically syncing transaction data from your ecommerce platform into your accounting software, eliminating manual data entry. Middleware tools like A2X parse lump-sum payouts from platforms such as SHOPLINE, Shopify, or Amazon into categorized journal entries: sales, fees, refunds, and shipping income.

Key functions these integrations perform include:

For brands selling across multiple channels, choosing a platform with a shared data layer reduces the number of reconciliation points your accounting software must handle.

You should hire a bookkeeper or ecommerce CPA when transaction volume, multi-state tax obligations, or inventory complexity exceed what you can accurately manage yourself. Common triggers include crossing economic nexus thresholds in multiple states, preparing for an audit, or needing accrual-basis financials for investors.

According to a 2024 report by Talentfoot, specialist ecommerce accounting positions require an average of 73 days to fill in the U.S. due to a CPA shortage. This scarcity means starting your search early matters. A general bookkeeper handles day-to-day categorization and reconciliation, while an ecommerce CPA addresses sales tax compliance, revenue recognition under ASC 606, and strategic tax planning.

With the right tools and professional support in place, consolidating your commerce data creates even greater accounting efficiency.

Unified commerce data changes your accounting workflow by consolidating orders, subscriptions, POS transactions, and inventory into one real-time data source. This eliminates manual reconciliation across disconnected systems and reduces compliance risk.

When orders, subscriptions, and POS live in one system, accounting shifts from reconciling multiple data exports to working with a single, shared record of every transaction. According to Salesforce, unified commerce integrates digital commerce, point-of-sale, and order management systems into a single platform, providing shared, real-time data.

Key workflow changes include:

For brands operating across B2B and DTC channels, this unified data model eliminates the duplicate entries and timing mismatches that create audit exposure. Small businesses face penalties up to $25,000 for non-compliant e-commerce operations, making data accuracy a compliance necessity rather than an operational luxury.

The key takeaways about ecommerce accounting are:

Accurate ecommerce accounting protects margins, supports clean audits, and gives operators the visibility needed to scale with confidence.